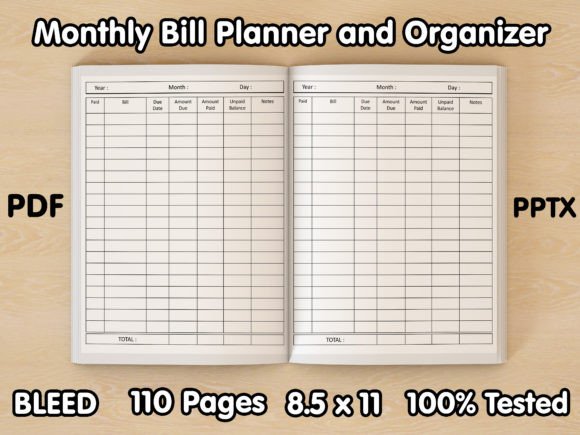

Master Your Finances with a Monthly Bill Payment Organizer

Managing household or business finances often feels like juggling with too many balls in the air. Due dates scatter across different statements, amounts vary, and that nagging uncertainty about what’s been paid can drain mental energy. This is where the simple, powerful tool of a dedicated bill payment organizer transforms chaos into clarity. A physical planner, like this 110-page, 8.5 x 11-inch notebook, isn’t just a ledger; it’s a command center for your financial flow.

What makes this approach interesting and profoundly useful is its tangible, focused nature. Unlike a digital spreadsheet that sits among countless tabs, a dedicated bill payment tracker is a singular space for a singular task. Each month, you confront your obligations on paper, which demands a different kind of attention and commitment. The act of writing “Amount Paid” and seeing the “Unpaid Balance” shrink provides a concrete sense of progress and control that a fleeting digital notification often lacks.

The Core Framework: From Checklist to Insight

The organizer’s typical layout—with fields for the bill’s name, due date, amount due, amount paid, unpaid balance, and notes—is a brilliant framework for basic tracking. But its real power lies in how you use that framework creatively to serve your specific financial picture. This isn’t just about recording; it’s about interpreting your spending patterns.

For instance, the “Notes” column is a canvas for insight. Instead of just writing “paid,” you could annotate patterns: “Higher this month due to summer AC use,” or “Switched to autopay, note new confirmation number.” Over time, these notes become a qualitative log that explains the quantitative data, helping you anticipate fluctuations and make informed adjustments. The “Bill Payments Checklist Box” at the start of each month’s section can be used not just as a to-do list, but as a priority map, color-coding or numbering bills by their importance or impact on your services.

Adapting the Planner for Different Lives and Goals

The beauty of this physical organizer is its flexibility. Different users can adapt the same 110 pages to radically different financial landscapes.

A freelance designer or blogger, whose income might be variable and projects client-based, could use each page not just for utilities, but to track project-related expenses and invoice due dates. They might create a hybrid system, using one side of the spread for personal bills and the other for business outflows, turning the organizer into a holistic financial dashboard. The “Unpaid Balance” column could cleverly track outstanding client payments alongside personal debts, offering a complete picture of cash flow.

A small business owner might dedicate entire sections of the book to recurring operational expenses: software subscriptions, inventory payments, loan installments, and payroll taxes. Here, the organizer scales from a household tool to a lightweight business accounting companion. The large 8.5 x 11 size offers ample space for detailed notes on vendor contacts or payment terms.

Even for a household focused on savings goals, the tracker can evolve. Beyond logging payments, you could add a small margin on each page to calculate the total monthly outflow versus income, tracking the surplus. This turns a bill payment organizer into a rudimentary budget snapshot, visually linking bill management to broader financial health.

Creative Extensions and Project Ideas

Think of the organizer as a foundational tool. Its structured pages can inspire related financial projects that deepen your control and creativity.

- Annual Forecast Project: Use the final pages of the book to create a simple annual summary. Each month, transfer your total bill payments to an annual chart. This visual project, built from monthly data, reveals seasonal spending trends and provides hard data for next year’s budget planning.

- Payment Method Audit: In your notes, track the payment method used (e.g., credit card A, bank transfer, autopay). After a few months, review to see if you’re optimizing rewards cards or simplifying methods. This turns tracking into a strategic review.

- Financial Simplification Log: Use the organizer as a catalyst for reduction. As you record each bill, ask if it’s essential. The notes column can become a log of canceled subscriptions or negotiated rates, documenting your journey to a simpler financial footprint.

Keeping It Clear, Consistent, and Effective

To reap the full benefits, consistency is key. The practical guidance is straightforward: designate a time each week, perhaps right after mail arrives or on a Sunday evening, to update your organizer. Treat it not as an chore, but as a brief financial review session. Keep a pen glued to the book and store it with your incoming bills or financial documents, so it’s physically part of the process.

For clarity, use simple abbreviations or codes that make sense to you. The goal is speed and accuracy of entry. The large page size allows for clear, uncluttered writing—avoid cramming text; use the space to keep entries readable. If you share finances with a partner or family, the organizer can become a shared communication tool, left open on a desk where updates are visible to all responsible parties, promoting transparency and shared responsibility.

From Tracking to Strategic Financial Awareness

Ultimately, this monthly bill planner and organizer is more than a tracker. It’s a practice that builds financial awareness and intentionality. The regular, tactile engagement with your outflows fosters a more mindful relationship with money. You see, in your own handwriting, where it goes each month. This awareness is the first and most crucial step toward better financial decisions, whether that’s cutting costs, saving for a goal, or simply eliminating the anxiety of forgotten payments.

For the entrepreneur, it brings business expenses into sharp focus. For the household, it turns a scattered pile of bills into a managed system. For the freelancer navigating variable income, it provides stability and predictability in outflows. The 110 pages offer a year’s journey, or more, of financial data collected in one accessible, offline, reliable place. In a digital world, this analog tool provides a focused, uninterrupted space to command the fundamental art of paying what you owe, on time, and with full knowledge. That control is not just practical; it’s profoundly empowering.